Last updated: 30 April 2026

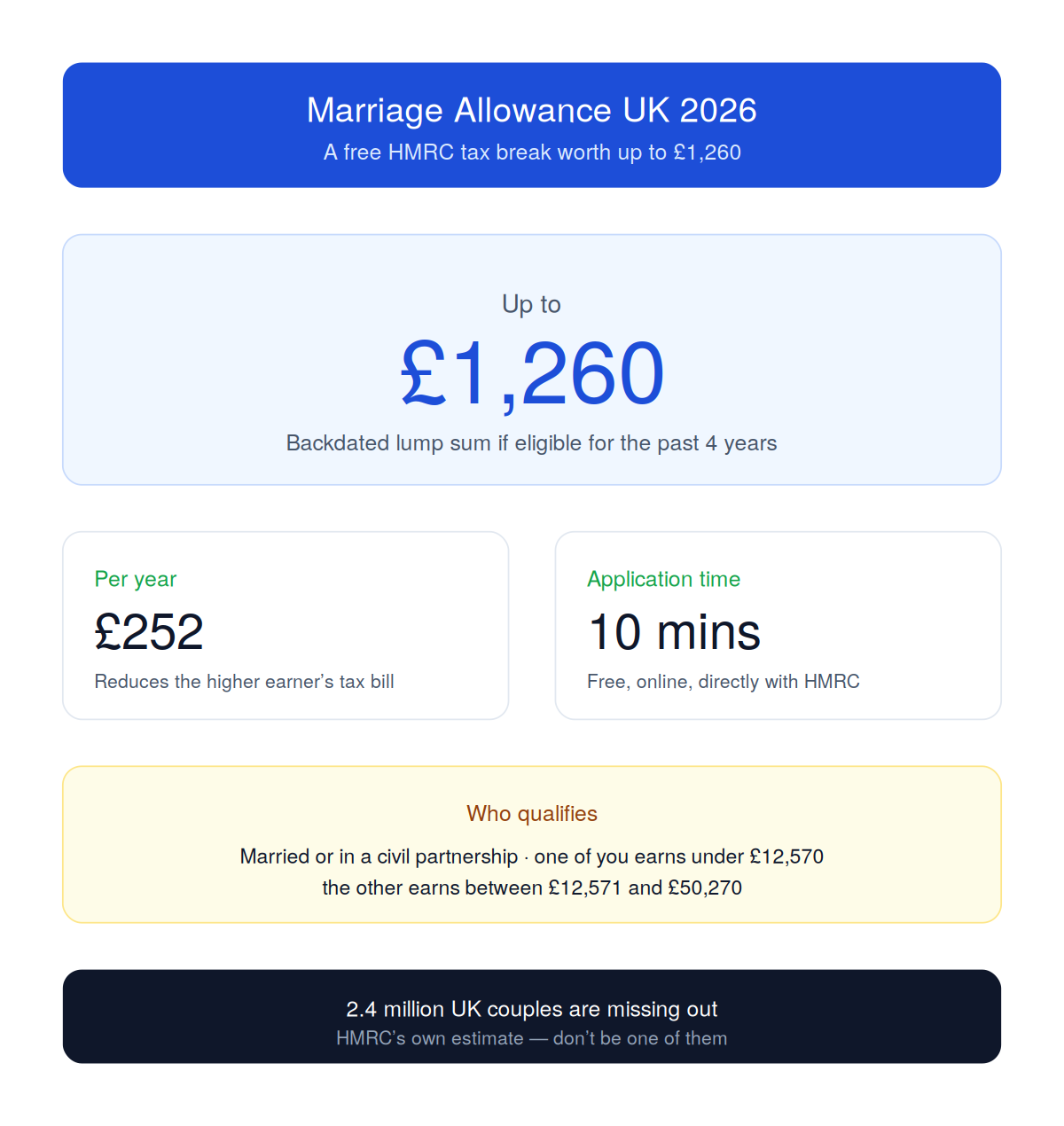

If you’re married or in a civil partnership and one of you earns less than the other, there’s a tax break worth up to £252 a year that around 2.4 million eligible couples never claim. It takes 10 minutes to apply, costs nothing, and you can backdate it by four tax years for a one-off lump sum of up to £1,260.

Yet most people either haven’t heard of Marriage Allowance, assume they don’t qualify, or end up paying a “tax refund firm” 30%+ of their refund to handle a form that’s genuinely simpler than online banking.

This guide walks you through it from the ground up — who qualifies, how the maths actually works, what the catches are, and exactly how to apply directly to HMRC for free.

What is Marriage Allowance?

Marriage Allowance is a tax break for married couples and civil partners where one person earns under the personal allowance threshold (£12,570 in 2026/27) and the other is a basic-rate taxpayer.

It works by letting the lower-earning partner transfer £1,260 of their unused personal allowance to the higher-earning partner. That extra allowance reduces the higher earner’s tax bill by up to £252 per year.

The lower earner doesn’t lose anything — they weren’t using that £1,260 of allowance anyway, because their income is below the tax-free threshold.

It’s been around since April 2015 but stays massively under-claimed. HMRC’s own estimate puts the number of eligible couples missing out at over 2 million.

Who can claim Marriage Allowance in 2026/27?

You can claim if all of the following are true:

- You’re married or in a civil partnership (cohabiting partners do not qualify, no matter how long you’ve lived together)

- One of you earns less than the personal allowance — under £12,570 a year in 2026/27

- The other partner is a basic-rate taxpayer — earning between £12,571 and £50,270 (or £43,662 if they live in Scotland)

- You were both born on or after 6 April 1935 (different rules apply to couples born before that — see “Married Couple’s Allowance” below)

If the higher-earning partner pays tax at the higher rate (40%) or additional rate (45%), you cannot claim. Marriage Allowance is specifically for couples where the higher earner is in the basic-rate band.

What about Scotland?

Scottish income tax bands are different. To qualify, the higher-earning partner needs to be a Scottish basic-rate taxpayer — so their income must be under £43,662 in 2026/27. The £252 saving and £1,260 transfer figures are the same as the rest of the UK.

How much is it worth?

In 2026/27 the maximum saving is £252 per tax year. That’s £1,260 of allowance transferred at the basic rate of 20% = £252.

But here’s where it gets more interesting: you can backdate your claim by up to four tax years, provided you were eligible during those years. Combined with the current year, that’s potentially:

- 2026/27: up to £252

- 2025/26: up to £252

- 2024/25: up to £252

- 2023/24: up to £252

- 2022/23: up to £252

Maximum total: £1,260 as a lump-sum refund, plus your tax bill reduced going forward.

The deadline matters. From 6 April 2026 onwards, the earliest tax year you can claim for is 2022/23. Anything earlier than that is now out of time.

A worked example

Sarah works full-time and earns £28,000 a year. Her husband Tom looks after their two children and works part-time, earning £6,500 a year.

Tom’s income is well below the £12,570 personal allowance, so he pays no income tax and isn’t using £6,070 of his allowance.

Tom applies to transfer £1,260 of his unused allowance to Sarah. HMRC adjusts Sarah’s tax code from 1257L to 1383M. Her personal allowance increases from £12,570 to £13,830, meaning £1,260 less of her income is taxed at 20% — saving her £252 a year.

If Sarah and Tom have been eligible for the past four tax years and never claimed, they’ll also receive a backdated lump-sum refund of around £1,000 covering 2022/23 through 2025/26.

When Marriage Allowance might not be worth it

Most eligible couples benefit, but there are edge cases where transferring the allowance can leave you slightly worse off.

If the lower earner’s income is between £11,310 and £12,570: transferring £1,260 reduces their personal allowance to £11,310. If they earn more than that, they’ll start paying a small amount of tax themselves. The higher earner still saves £252, but the lower earner might pay up to £252 in new tax — cancelling out the gain.

As a rule of thumb: if the lower earner’s income is below £11,310, the couple gets the full benefit. If it’s between £11,310 and £12,570, run the numbers carefully — or use a calculator before applying.

If the higher earner’s income is right at the basic-rate threshold: receiving the extra allowance shouldn’t push you into higher-rate tax (the calculation accounts for this), but check carefully if your income fluctuates.

How to apply — the free way

The lower-earning partner is the one who needs to apply. You can do this in three ways:

1. Online (current year only — fastest)

Go to GOV.UK’s free Marriage Allowance application: https://www.gov.uk/apply-marriage-allowance

You’ll need:

- Your National Insurance number

- Your partner’s National Insurance number

- A way to prove your identity (passport, P60, or details from a recent payslip)

This route only applies for the current tax year. If you want to backdate, see option 2.

2. By post (for backdating to previous years)

If you want to claim for previous years as well, you’ll need to apply by post using the Marriage Allowance Transfer Claim form (MATCF). You can request this from HMRC by calling 0300 200 3300, or download it from GOV.UK. This single form covers both the current year and previous tax years.

3. By phone

Call HMRC on 0300 200 3300. Useful if the online form isn’t working or you prefer to talk to someone, but expect a wait.

You don’t need to reapply every year. Once Marriage Allowance is in place, it carries over automatically each tax year unless you cancel it or your circumstances change.

Don’t pay a “refund firm” for this

A whole industry of third-party “tax refund companies” advertises Marriage Allowance claims, taking 30–50% of any refund as their fee.

For a £1,260 backdated claim, that’s up to £600 in fees — for filling in a form that takes 10 minutes and asks for nothing more than your National Insurance number.

HMRC’s own service is free, the form is straightforward, and the refund goes directly into your bank account. There is no scenario in which using a paid refund firm is the right move for a Marriage Allowance claim.

What happens after you apply?

Once HMRC processes your claim:

- The lower earner’s tax code changes to one ending in N (e.g. 1131N) — this means they’ve transferred part of their allowance

- The higher earner’s tax code changes to one ending in M (e.g. 1383M) — this means they’ve received the transfer

- The higher earner’s monthly take-home pay goes up by around £21

- Any backdated refund is paid as a lump sum, by cheque or bank transfer, within 6–8 weeks

You don’t need to do anything in subsequent tax years — the allowance carries over automatically.

What if circumstances change?

If you separate or divorce: Marriage Allowance continues until the end of the tax year in which you formally separate. After that, you’ll need to cancel it by contacting HMRC.

If one of you starts earning above the higher-rate threshold: the higher earner becomes a higher-rate taxpayer and is no longer eligible. You should cancel the claim — otherwise HMRC will catch up later and ask for the money back.

If your partner dies: the surviving partner can still claim Marriage Allowance for tax years where both partners were alive and eligible.

Married Couple’s Allowance vs Marriage Allowance — what’s the difference?

These two things sound similar but are completely different.

Marriage Allowance (this guide) is for couples where one partner earns under the personal allowance. Worth up to £252 a year. Applies to anyone born on or after 6 April 1935.

Married Couple’s Allowance (MCA) is a separate, older tax break only available where at least one partner was born before 6 April 1935 (so they were aged 91 or over at the start of 2026/27). It’s worth up to £1,170 a year in 2026/27. Different rules, different application route.

If you were born after 1935, Marriage Allowance is the one to look at.

Quick check before you apply

Before you start the application, run through this short checklist:

- Are you married or in a civil partnership? (not just living together — this matters)

- Does the lower earner make under £12,570 in 2026/27?

- Does the higher earner make between £12,571 and £50,270 (or £43,662 in Scotland)?

- Were you both born on or after 6 April 1935?

- Have you been eligible in any of the four previous tax years (2022/23 onwards)?

If you tick the first four, you can claim £252 for the current year. If you also tick the last one, you may have a backdated refund of up to £1,008 on top.

Try our free Marriage Allowance calculator

Not sure exactly how much you could be owed? Use our free Marriage Allowance Refund Calculator to get an instant estimate based on your income and how many years you can backdate. No sign-up, no email required.

Last updated: April 2026 (for the 2026/27 tax year). This guide is for general information only and not personal tax advice. For HMRC’s official guidance, see gov.uk/marriage-allowance.